You are here: Symbol Reference > StatTimeSerAnalysis Namespace > Functions > StatTimeSerAnalysis.TripleExpSmooth Function

|

Stats Master VCL

|

|

|

StatTimeSerAnalysis.TripleExpSmooth Function

|

Stats Master VCL

|

|

|

Triple exponential smoothing.

|

Parameters |

Description |

|

Y |

Time series data set. |

|

S |

Smoothed values (see above equation). Size and complex properties of S are set automatically. |

|

B |

Trend values (see above equation). Size and complex properties of b are set automatically. |

|

L |

Seasonal indices (see above equation). Size and complex properties of L are set automatically. |

|

Alpha |

Defines initial estimate for Alpha, returns Alpha which minimizes MSE. |

|

Beta | |

|

Gamma | |

|

Period |

Period length. An exception is raised if Y.Length mod Period is not 0. |

MSE, evaluated at minimum.

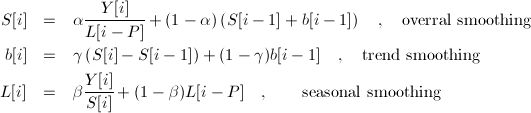

Performs triple exponential smoothing (also known as Holt-Winters smoothing) using the following equations:

where Y are the observations, S are the smoothed observations, b trend factors, L the seasonal indices and P is the period length. To initialize triple exponential smoothing method we need at least one complete season's data to determine initial estimates of the seasonal indices L[0]..L[P-1]. Again, there are several ways to initialize L values. The algorithm uses approach, described at www.itl.nist.gov/div898/handbook/pmc/section4/pmc435.htmpage. For initial estimate for S and b, the following equations are being used:

There are no S[0]..S[P-2] values; the smoothed series starts with the smoothed version of the Y[P] observation. Also note that the internal algorithm automatically accounts for this by resizing S,b vector to Y.Length-Period.

Generate 24 random values representing 4 quarters x 6 years = 24, perform smoothing and read Alpha,Beta,Gamma + MSE.

Uses MtxExpr,StatTimeSerAnalysis, Math387; procedure Example; var Data,S,b,L: Vector; Alpha,Beta,Gamma,MSE: double; begin Data.Size(24,false); Data.RandGauss; // smooth data, initial alpha = 0.1, beta=0.1, gamma = 0.3 Alpha := 0.1; Beta := 0.1; Gamma := 0.3; // Period = 4 MSE := TripleExpSmooth(Data,S,b,L,Alpha,Beta,Gamma,4); // results: MSE and MLE estimate for Alpha,Beta,Gamma end;

#include "MtxExpr.hpp" #include "Math387.hpp" #include "StatTimeSerAnalysis.hpp" void __fastcall Example(); { sVector Data,S,b,L; Data.Size(24,false); Data.RandGauss(); // smooth data, initial alpha = 0.1, beta=0.1, gamma = 0.3 double alpha = 0.1; double beta = 0.1; double gamma = 0.3; // Period = 4 double MSE = TripleExpSmooth(Data,S, b, L, alpha,beta,gamma,4); // results: MSE and MLE estimate for Alpha,Beta,Gamma }

|

Copyright (c) 1999-2025 by Dew Research. All rights reserved.

|

|

What do you think about this topic? Send feedback!

|

File

File