You are here: Symbol Reference > StatTimeSerAnalysis Namespace > Functions > StatTimeSerAnalysis.BoxLjung Function

The box-Ljung statistics.

function BoxLjung(const X: TVec; const h: Integer): double;

|

Parameters |

Description |

|

X |

Defines the residuals of predicted values. |

|

h |

Defines the number of lags used in statistics. |

the Box-Ljung statistics.

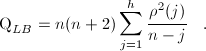

The Ljung-Box test is based on the autocorrelation plot. However, instead of testing randomness at each distinct lag, it tests the "overall" randomness based on a number of lags. For this reason, it is often referred to as a "portmanteau" test. The Ljung-Box test statistics can be defined as follows:

where n is the sample size, rho(j) is the autocorrelation at lag j, and h is the number of lags being tested. Actually we are testing the hypothesis:

The Ljung-Box test is commonly used in ARIMA modeling. Note that it is applied to the residuals of a fitted ARIMA model, not the original series.

|

Copyright (c) 1999-2025 by Dew Research. All rights reserved.

|

|

What do you think about this topic? Send feedback!

|

File

File